The way airlines distribute their content is changing — and for Travel Management Companies (TMCs), the stakes could not be higher. Two technologies sit at the centre of this shift: the Global Distribution System (GDS) and the New Distribution Capability (NDC). Understanding the difference between GDS vs NDC is no longer optional for TMC operators. It is the difference between offering your corporate clients competitive fares and missing content that only lives on direct airline channels.

The way airlines distribute their content is changing — and for Travel Management Companies (TMCs), the stakes could not be higher. Two technologies sit at the centre of this shift: the Global Distribution System (GDS) and the New Distribution Capability (NDC). Understanding the difference between GDS vs NDC is no longer optional for TMC operators. It is the difference between offering your corporate clients competitive fares and missing content that only lives on direct airline channels.

This article breaks down how each system works, where they diverge, and what a smart dual-source strategy looks like for a modern TMC.

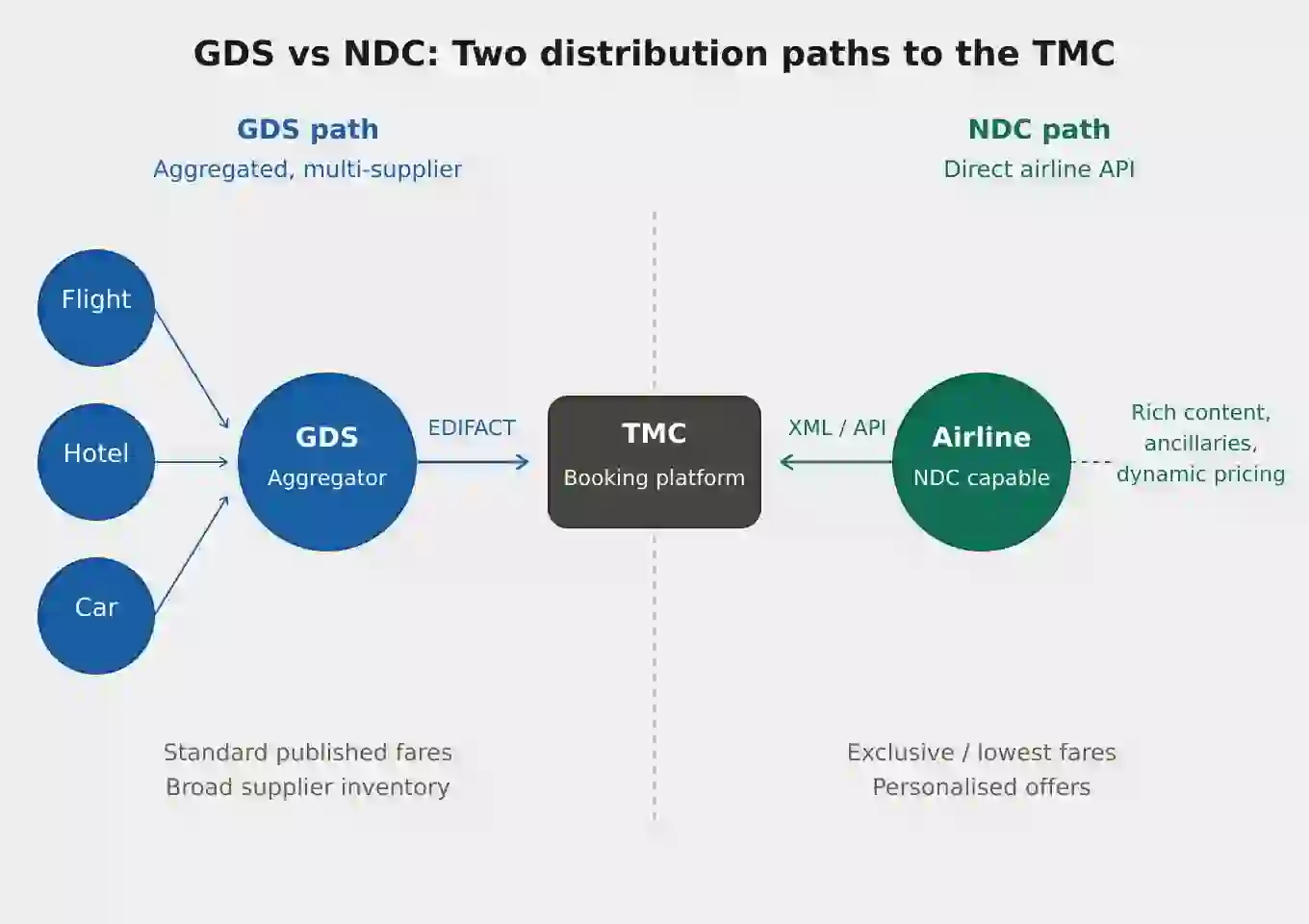

What Is a GDS?

A Global Distribution System is a centralised technology network that connects airlines, hotels, car rental companies, and other travel suppliers with travel agents and booking platforms. The major GDS providers are Amadeus, Sabre, and Travelport.

GDS technology traces its roots to the 1960s, when airlines built their first Computer Reservation Systems (CRS). By the 1990s, these had evolved into multi-supplier networks capable of aggregating inventory from thousands of providers into a single query. Today, GDS remains the backbone of most TMC booking workflows.

For a deeper look at how GDS works, see our article: What Is GDS in Travel?

What Is NDC?

NDC — New Distribution Capability — is an XML-based data transmission standard introduced by the International Air Transport Association (IATA) in 2012. It was designed to address a fundamental limitation of GDS: the legacy EDIFACT protocol could not carry rich airline content such as seat maps, ancillary offers, images, or personalised pricing.

Under NDC, airlines communicate directly with travel sellers using modern API technology. This allows them to offer bundled fares, dynamic pricing, upsell ancillaries (baggage, lounge access, Wi-Fi), and loyalty programme integration — all in a single transaction flow.

Want the full background? Read: What Is NDC in Travel?

GDS vs NDC — Key Differences

The table below summarises the most important distinctions for TMC operations:

| Feature | GDS (EDIFACT) | NDC (XML/API) |

|---|---|---|

| Data standard | Legacy EDIFACT | Modern XML |

| Airline coverage | Very broad | Growing; not all airlines |

| Fare access | Standard published fares | Exclusive / lowest fares |

| Dynamic pricing | No | Yes |

| Rich content (images, video) | No | Yes |

| Ancillary services | Limited | Full (bags, seats, meals, Wi-Fi) |

| Distribution surcharge | Yes (GDS booking fee) | No |

| Personalisation | No | Yes |

| Changes & exchanges | Well-supported | Improving; varies by airline |

| Implementation complexity | Low (mature tooling) | High (API integration needed) |

Why NDC Matters More for TMCs Now

Airlines are actively moving their best content off GDS. For TMCs, this creates a real commercial problem: if your booking platform does not connect to NDC channels, your corporate clients may be paying more than they need to — and your agency may be losing the deals to competitors who have made the switch.

The numbers make this concrete. Singapore Airlines has made its NDC programme (KrisConnect) a centrepiece of its distribution strategy. NDC fares are approximately 6% lower than equivalent GDS fares, and corporate fares run around 7% lower. From September 2025, certain discounted cabin classes are only available via NDC — they are not accessible through GDS at all.

Source: Singapore Airlines NDC / KrisConnect

This trend is not limited to Singapore Airlines. Across the industry, carriers are using NDC to offer differentiated products — exclusive bundles, seat upgrades, loyalty miles — that simply cannot be replicated over a standard GDS pipe. For TMCs managing high-volume corporate accounts, the savings and content gap compounds quickly

The Case for Keeping GDS

Despite the momentum behind NDC, GDS remains essential for most TMC workflows — and abandoning it prematurely would be a mistake.

Here is why GDS still matters:

• Breadth of inventory: GDS connects to thousands of airlines, hotels, and car rental providers. NDC coverage is still concentrated in major carriers and varies significantly by region.

• Reliability and maturity: Decades of development means GDS tooling for ticketing, exchanges, refunds, and queue management is robust and well-understood by agents.

• Mid-office integration: Most TMC back-office systems — PNR management, reporting, duty of care — are built around GDS data structures. Replacing this infrastructure overnight is not realistic.

• Multi-carrier itineraries: Complex itineraries involving multiple airlines are still easier to construct and manage through GDS, particularly where interline agreements are involved.

In short, GDS is a proven system with unmatched reach. The question is not whether to replace it, but how to extend beyond it.

The Asia-Pacific Angle: Why This Matters More Here

Asia-Pacific is not just keeping pace with the global NDC shift — in many ways, the region is defining it. For TMCs headquartered in Southeast Asia, Greater China, or the Indian subcontinent, the GDS vs NDC question carries distinct regional dimensions that European and North American playbooks do not fully address.

Major APAC Carriers Are Moving Fast

Several of the region's flagship carriers have made NDC a core part of their distribution strategy:

• Singapore Airlines (KrisConnect): Among the most advanced NDC programmes globally, certified under IATA's Airline Retailing Maturity (ARM) Index. NDC fares average 6% lower than GDS equivalents, with corporate fares running 7% lower. As of September 2025, select discounted cabin classes are only available via NDC.

• Cathay Pacific: Expanding NDC access through a multi-year content agreement with Travelport, making NDC content available to travel agencies via Travelport Plus. Cathay's NDC offering includes intermodal options — a capability few carriers globally have implemented.

• Philippine Airlines (PAL): Launched a dynamic booking and selling platform powered by NDC via Amadeus, enabling richer personalisation of ancillaries and seat selections for travel partners.

• ANA (All Nippon Airways): Investing in NDC as part of a broader digital transformation strategy across its Japan-centric and international network.

Amadeus has also signed NDC partnerships with regional online travel agencies including tiket.com (Indonesia's first OTA to adopt NDC in Southeast Asia) and ezTravel (Taiwan's largest OTA), reflecting how rapidly NDC infrastructure is spreading across the distribution chain.

The LCC Factor: A Unique APAC Challenge

Asia-Pacific has one of the highest proportions of low-cost carrier (LCC) traffic of any region. Airlines like AirAsia, Scoot, Cebu Pacific, and IndiGo have long operated outside traditional GDS channels — many distributing exclusively through their own websites or direct API connections. This means TMCs in the region have always had to manage a multi-source content problem that their Western counterparts are only now encountering with NDC.

For APAC TMCs, the transition to a dual-source model is therefore less of a conceptual leap and more of a formalisation of something they have been navigating informally for years. The difference now is that full-service carriers are joining the direct-channel movement — and the content gaps are becoming commercially significant.

Regional Market Fragmentation

Asia-Pacific is not a single market. A TMC managing corporate travel across Singapore, Malaysia, Indonesia, the Philippines, and Japan is dealing with different airline landscapes, different GDS penetration rates, and different NDC readiness levels in each country. GDS coverage can be uneven on intra-regional routes, particularly for secondary city pairs where LCCs dominate.

This fragmentation makes a technology platform decision particularly consequential for APAC TMCs. A booking tool that handles NDC for major hub-to-hub routes while falling back to GDS for broader regional inventory — without requiring agents to switch systems — is not a luxury. It is an operational necessity.

Asia-Pacific NDC market size reached USD 420 million in 2024, with the region forecast to grow faster than the global average through 2033.

Source: Growth Market Reports

A Dual-Source Strategy for TMCs

The most forward-looking TMCs are not choosing between GDS and NDC — they are running both in parallel. A dual-source strategy means your booking platform queries GDS and NDC content simultaneously, then presents the best available option to the traveller or travel manager.

What this looks like in practice:

• GDS handles the bulk of multi-carrier, hotel, and car rental inventory.

• NDC connections to key airlines (e.g. Singapore Airlines, British Airways, Lufthansa Group) surface exclusive fares and ancillary bundles that GDS cannot see.

• The booking interface normalises both content types so agents and travellers do not need to know — or care — where the content originated.

• Reporting and mid-office systems capture both GDS PNRs and NDC order references in a unified view.

This approach maximises value: the breadth of GDS combined with the pricing advantages and richer content of NDC. For corporate travel programmes with significant volume on NDC-active airlines, the cost savings alone justify the investment in dual-source capability.

TMCs looking to understand where they sit in the broader ecosystem should also read: What Is a Travel Management Company?

How the Right Booking Platform Makes This Seamless

The practical challenge with a dual-source strategy is integration complexity. NDC API connections require technical investment — implementation timelines can run six months to a year per airline. Managing this alongside existing GDS workflows, mid-office systems, and corporate travel policies is a significant operational undertaking.

This is where platform choice becomes critical. A corporate booking tool built with NDC-readiness in mind abstracts away that complexity — giving travel managers and agents a single interface that surfaces GDS and NDC content side by side, enforces policy compliance regardless of content source, and feeds clean data into reporting and back-office workflows.

Forecepts' Corporate Booking Tool is built for exactly this scenario — helping TMCs serve corporate clients with access to competitive fares and richer content, without the operational overhead of managing multiple disconnected systems.